This article forms part of our wider Budget 2021 coverage including expert analysis of the tax aspects which can be found on our Budget Hub.

For the Financial Institutions sector the Autumn Budget did not contain any significant surprises, although the expected reduction of the bank corporation tax surcharge mitigated the risk of the sector facing a significant increase in tax burden and aligns the sector more closely with the main corporation tax rate once the main rate increases to 25% from April 2023. Some of the measures which may have the largest impact in the long term, such as potential changes to stamp duty and stamp duty reserve tax in a securitisation context and a new re-domiciliation regime, are still in the early stages but are welcome signs for the industry. We've highlighted some of the key changes and proposals impacting the sector specifically below.

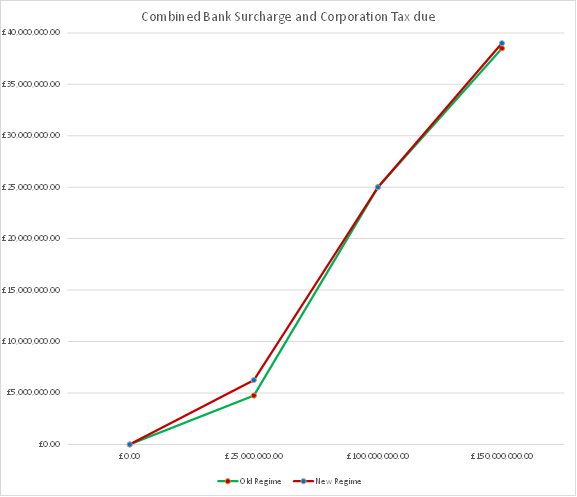

The prospect of the bank surcharge of 8% applying on top of the of the 6% increase in the main corporation tax rate was never likely to be realised given the cumulative tax rate of 33% would be internationally uncompetitive. The Treasury has opted to decrease the surcharge from 8% to 3% and increased the threshold for the bank surcharge to apply from £25m to £100m to partially mitigate these measures. The overall tax due will however universally be higher under the new measures. This is because the initial £25m will be subject to the increase in the main corporation tax rate whilst it was not subject to the bank surcharge. The marginal rate of tax under the old measures would have been higher on profits between £25m and £100m but this does not equal the additional tax due on the first £25m of profit until profit reaches £100m. The new 28% marginal rate of tax will then apply compared to the previous 27% marginal rate of tax, widening the gap between the two regimes.

HM Treasury has been granted powers to introduce secondary legislation to vary stamp duty and stamp duty reserve tax on notes issued by securitisation companies and insurance linked securities. Whilst the specific form of any such relief remains unclear, the current UK stamp duty and stamp duty reserve tax issues are a significant downside for UK securitisation and insurance linked security vehicles compared to competitor regimes, such as those in Ireland and Luxembourg. We expect HM Treasury and HMRC to consult extensively on the form of any statutory instruments which may result in more suitable legislation than that included in a headline Finance Bill.

Whilst not of immediate impact the long term consequences of the introduction of a re-domiciliation regime could be significant. A re-domiciliation regime would allow a company to change its country of incorporation to the UK whilst retaining its trading and corporate history. Any regime would still require the outbound country to have a similar scheme and whilst approximately 50 countries have introduced such a scheme, a number are "inbound" only. Consultation responses are requested by the 7thJanuary 2022.

The introduction of the uncertain tax treatment measures is unlikely to cause significant issues for entities already covered by the Code of Practice on Taxation for Banks but those financial institutions which fall outside the code will need to consider the introduction of the regime in more depth. Identifying those tax risks with a provision in the accounts will be relatively straightforward but the second trigger, tax positions taken which are not in accordance with HMRC's view, may be more difficult to identify. The measures apply for returns filed after 1st April 2022.

More positively, the government has confirmed its intention to increase access to R&D tax reliefs by expanding qualifying expenditure to include data and cloud costs. On the flip side, relief will be refocussed towards supporting innovation in the UK and measures will be introduced to target abuse and improve compliance. These changes will be legislated for in Finance Act 2022 and take effect from April 2023. Further details of these changes are still awaited and the Budget documents merely state that the next steps for the review will be set out in due course.

A technical but welcome change has been announced in response to the introduction of IFRS 17, the new international standard for insurance contracts. The government has proactively announced that regulations will be introduced allowing it to both provide for the transitional impacts of IFRS 17 to be spread for tax purposes and repeal the current requirement on life insurance companies to spread acquisition expenses over seven years for tax purposes. A consultation on the regulations will be launched in the coming weeks. Affected insurers and their advisers should consider responding to the consultation (when launched) to ensure that their views are taken into account.

The Dormant Asset Scheme has been expanded to cover additional asset classes such as pensions, insurance, investments, wealth management and securities. This Scheme enables assets in dormant accounts to be used for the public good whilst still remaining available to the unidentified account holder should they ultimately seek to claim the assets.

The review of the funds regime continues to consult on options to resolve the contentious issue of the VAT treatment of fund management fees. The current situation represents a competitive disadvantage to UK providers and recipients of discretionary investment management services.

Finally, the introduction of the economic crime levy which will apply to all financial institutions has been confirmed although the specific fixed fees payable by entities falling within the largest three (of four) revenue bands will be set out in the draft legislation.

Our full review of the all the most significant tax measures from yesterday's Budget can be found on our Budget pages.

_11zon.jpg?crop=300,495&format=webply&auto=webp)

.jpg?crop=300,495&format=webply&auto=webp)

_11zon.jpg?crop=300,495&format=webply&auto=webp)